How Do Charitable Lead Trusts Work?

For high-net-worth clients with complex charitable giving and wealth preservation needs, charitable lead trusts (CLTs) might offer a unique opportunity. CLTs enable families to direct income from their valuable assets to charity for a defined period, reduce their tax burdens, pass wealth to future beneficiaries, and retain their valuable assets for future use.

While CLTs are one of the more complex giving vehicles, they’re also one of the most powerful and underutilized strategies available for clients with substantial estates and charitable intent.

The basic concept is straightforward to explain to clients: a CLT functions like a temporary loan of an income-producing asset to charity. During the trust term, the charity receives income payments. At termination, the assets pass back to the client’s estate or to their heirs.

For families with the assets, the reasoning is simple: they support causes they care about, receive substantial tax benefits, and ultimately keep the assets in the family. Why would they kill the goose that lays golden eggs?

Continue reading for a high-level overview of whether CLTs might not benefit your clients, as well as some practical considerations for implementation. You can also call Greater Houston Community Foundation today at 713-333-2210 or reach out directly to start planning your client’s trust.

Key Insights

- A charitable lead trust allows clients to “loan” income-producing assets to charity for a set period, generating tax deductions and ultimately preserving the assets for heirs.

- Non-grantor CLTs are the more common structure because they often better allow clients to leverage their gift tax exemption and transfer significantly more wealth.

- Unlike charitable remainder trusts, CLTs are not tax-exempt entities—trust income faces taxation, making asset selection and retention strategies essential.

- Pairing a CLT with a donor advised fund at a community foundation provides flexibility to adjust charitable beneficiaries over time without amending the trust document.

- CLTs require coordination among estate planning attorneys, tax advisors, and investment managers—this is not a do-it-yourself strategy, but Greater Houston Community Foundation can partner with your advisory team to implement the charitable component.

Table of Contents

- What is the main reason for setting up a charitable lead trust?

- How does a charitable lead trust work?

- How do charitable lead trust tax deductions work?

- Charitable lead trusts pros and cons

- Charitable lead trust example: pairing CLTs with DAFs

- Charitable lead trust FAQs

- Partner with the Community Foundation on your client’s charitable lead trust

What is the main reason for setting up a charitable lead trust?

The threshold question is simple: does your client own an income-producing asset they ultimately want to pass to family members? If so, a CLT may be a good option for them. Charitable lead trusts can be particularly attractive if your clients face potential gift or estate tax exposure.

The most common reasons for clients to set up a CLT include:

- They hold significant appreciated, income-producing assets (securities, real estate, business interests)

- They have used or expect to exceed their lifetime gift tax exemption

- They have established charitable intent and specific organizations they wish to support

- They can forgo access to the transferred assets for the trust term

- They have sufficient liquidity outside the trust for living expenses

For these clients, a CLT offers a compelling value proposition: leverage the tax benefits of charitable donations to trusts, provide substantial support to charity, and ultimately transfer significantly more wealth to heirs than would be possible through direct gifts.

How does a charitable lead trust work?

While CLTs can get incredibly complex, the high-level view of their functionality includes three phases.

| Phase 1: Funding the trust |

| The client transfers property to an irrevocable trust. Suitable assets often include publicly traded securities, income-producing real estate, or closely held business interests. Many clients choose to donate stock in charitable planning. Unlike charitable remainder trusts, charitable lead trusts do not provide a capital gains tax exemption on the sale of assets; capital gains are taxable either to the trust (in a non-grantor CLT) or to the grantor (in a grantor CLT). |

| Phase 2: Charitable income payments |

| During the trust term (often 10–20 years, though terms can be shorter), the trust makes payments to designated charities. The payment structure follows one of two models: a charitable lead annuity trust (CLAT) pays a fixed dollar amount annually, while a charitable lead unitrust (CLUT) pays a fixed percentage of annually revalued trust assets. |

| Phase 3: Remainder distribution |

| At the end of the trust, remaining assets pass to the designated remainder beneficiaries—typically the donors themselves, children, or grandchildren, though dynasty trust structures can extend benefits further or to another charity or trust. |

The following table illustrates projected outcomes for a $5,000,000 CLT with a 10-year term and 5% annuity payout:

| Component | Calculation | Amount |

| Initial contribution | Value of original property | $5,000,000 |

| Annual distribution | 5% of $5,000,000 | $250,000 |

| Charitable deduction | Gift tax reduction | $1,968,500 |

| Taxable gift | Initial value ($5,000,000) minus deduction ($1,968,500) | $3,031,500 |

| Total to charity | Annual contribution over 10 years | $2,500,000 |

| Total trust to family | After tax and appreciation | $7,787,740 |

How do charitable lead trust tax deductions work?

The value of the asset’s charitable income stream can be treated as either an income tax deduction (grantor CLT) or work to reduce the taxable amount of the final gift (non-grantor CLT). These CLT deduction calculations can be more complex than many traditional tax write-offs on donations, but follow similar principles.

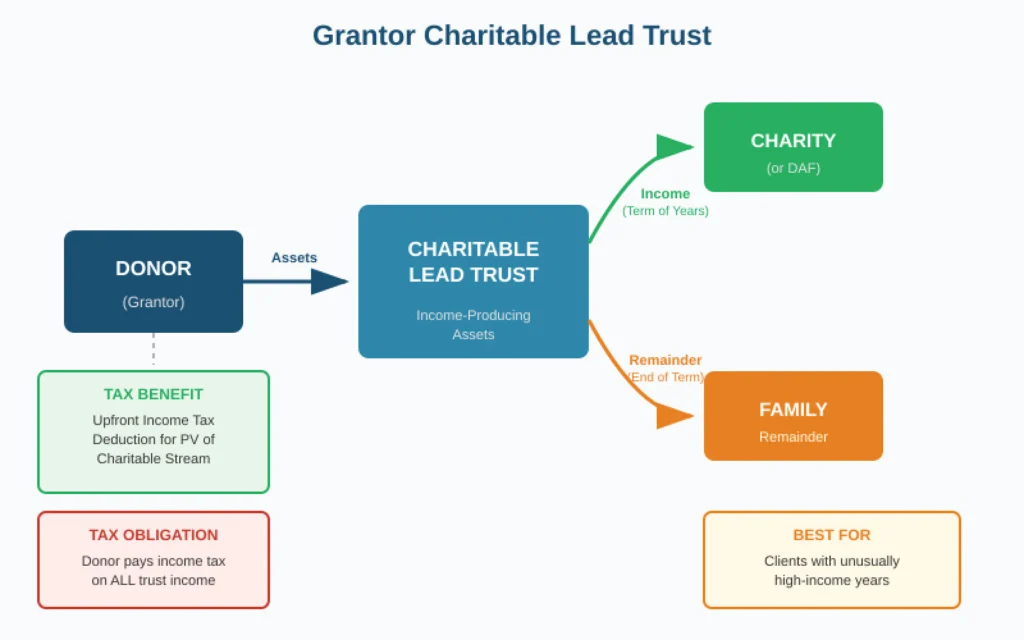

Grantor charitable lead trusts

When a CLT is structured as a grantor trust, the donor may claim an immediate income tax charitable deduction based on the present value of future payments destined for the charitable beneficiary. This upfront benefit comes with an ongoing obligation: the trust’s investment income remains taxable to the grantor throughout the entire trust term. The deduction calculation accounts for the trust duration, anticipated lead payments, and applicable IRS interest rates.

| This structure works best for clients experiencing an unusually high-income year who can absorb a substantial deduction immediately. |

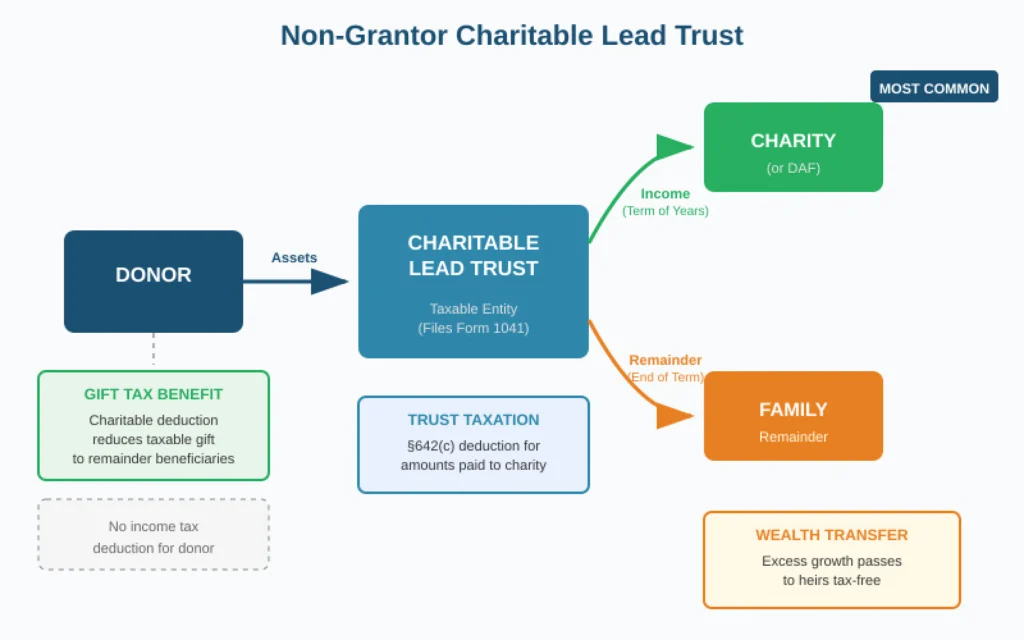

Non-grantor charitable lead trusts

With a non-grantor structure, the trust itself—rather than the donor—is treated as the owner of trust assets for tax purposes. The donor cannot claim an income tax deduction for the present value of the charitable lead interest. Instead, the trust pays tax on its undistributed net income and claims an unlimited income tax charitable deduction for distributions made to the charitable beneficiary.

When assets pass to successors at the end of the trust term, the donor’s estate qualifies for an estate tax charitable deduction based on the value of the interest paid to charity. This can meaningfully reduce estate tax liability while preserving wealth for the next generation. Similarly, lifetime contributions to a non-grantor CLT may qualify for a gift tax charitable deduction, potentially reducing or eliminating gift tax on the remainder interest passing to beneficiaries.

| The trade-off is worthwhile for most clients because non-grantor CLTs can deliver better transfer tax benefits. |

Charitable lead trusts pros and cons

If you’re currently evaluating whether or not a CLT is right for your client, you should weigh the following considerations:

CLTs offer several advantages that may be difficult to achieve through other strategies:

- Exemption leverage: CLTs may give you the ability to transfer significantly more wealth than the exemption amount used.

- Estate freeze characteristics: Post-gift appreciation occurs outside the donor’s estate.

- Substantial charitable impact: Charities receive meaningful, predictable funding over extended periods.

- Asset retention: Specific assets (family business interests, real estate) can remain in the family.

- Flexibility in charitable designation: Donors select beneficiary organizations, with ability to name DAFs for ongoing flexibility.

- Zeroed-out CLAT potential: Properly structured, transfers have the ability to be sheltered entirely by the charitable deduction, creating a taxable gift of zero.

CLTs do come with their fair share of considerations:

- Complexity and cost: Drafting, administration, annual tax filings, and trustee fees create ongoing expenses and coordination requirements.

- Irrevocability: Once funded, the transfer cannot be undone. Client circumstances may change over a 10–20 year term.

- Investment risk: Underperformance may reduce wealth transfer benefits.

- No capital gains bypass: Unlike CRTs, selling appreciated assets within the CLT triggers capital gains tax at trust rates.

- Basis carryover: Remainder beneficiaries receive the donor’s basis, potentially creating future capital gains liability.

For most planning situations, the sheer complexity of forming and administering a CRT will be the biggest barrier. They require coordination among estate planning attorneys, tax advisors, investment managers, and potentially corporate trustees—and close collaboration with philanthropic professionals with experience structuring these gifts.

Charitable lead trust example: pairing CLTs with DAFs

One particularly effective implementation strategy involves directing CLT income payments to a donor advised fund at the Community Foundation. Structuring CLT payments this way addresses one of the CLT’s inherent limitations: the requirement to name specific charitable beneficiaries for a trust term that may span decades.

Consider a 15-year CLAT directing $200,000 annually to the client’s donor advised fund at Greater Houston Community Foundation.

- Each year, the DAF receives its payment, and the client (or successor advisors) recommends grants to operating charities.

- If philanthropic priorities shift during the trust term, grant recommendations adjust accordingly without requiring trust modification.

- The DAF provides flexibility to respond to changing circumstances while maintaining the CLT’s tax structure.

- The community foundation handles grantee due diligence and compliance monitoring.

- The structure can facilitate family involvement in philanthropy, with successor generations participating in grant recommendations.

At trust termination, remainder assets pass to designated beneficiaries as planned. Some clients structure the remainder to fund a new DAF for the next generation, creating continuity of family philanthropy. Others coordinate CLT planning with donating retirement assets or qualified charitable distributions to create even more comprehensive charitable giving and wealth transfer plans.

Charitable lead trust FAQs

What is the difference between a CRT and a CLT?

You can think of charitable remainder trusts (CRTs) and charitable lead trusts (CLTs) as structural inverses.

| With a CRT, the donor or designated beneficiaries receive income for a term of years or life, with the remainder passing to charity. CRTs provide income tax deductions and capital gains deferral, serving primarily as income and retirement planning tools. |

| With a CLT, charity receives income first, and the remainder passes to non-charitable beneficiaries. CLTs provide gift/estate tax deductions (or income tax deductions for grantor CLTs), serving primarily as wealth transfer vehicles. |

The choice between the two often depends on whether the client’s priority is generating income (CRT) or transferring wealth to heirs (CLT).

What is the difference between a charitable lead trust and a charitable lead annuity trust?

“Charitable lead trust” is the general category; “charitable lead annuity trust” (CLAT) is one of two specific structures. A CLAT pays a fixed dollar amount to charity annually regardless of trust performance. A charitable lead unitrust (CLUT) pays a fixed percentage of annually revalued trust assets.

CLATs are more popular because they usually offer better wealth transfer potential: if trust returns exceed a minimum rate, all excess growth transfers to remainder beneficiaries tax-free. With a CLUT, higher returns increase charitable payments proportionally, reducing the wealth transfer benefit.

What is the 5% rule for trusts?

The 5% minimum payout requirement applies to charitable remainder trusts, not charitable lead trusts. CLTs have no minimum payout requirement. Payout rates do, however, significantly affect planning outcomes.

Lower payout rates increase the taxable gift (smaller charitable deduction) but leave more assets to grow for remainder beneficiaries. Higher payout rates reduce the taxable gift but generate less wealth transfer benefit. Most CLTs use payout rates between 5% and 8%, balancing these considerations against projected returns.

Does a charitable lead trust file a tax return?

Yes, all CLTs file Form 1041 annually, reporting all trust income and claiming deductions for charitable distributions and administrative expenses. With careful administration—or making sure charitable distributions and deductible expenses offset taxable income—most non-grantor CLTs minimize or eliminate income tax liability. If the trust holds assets generating income in excess of the charitable payout, trust-level taxation may result.

Partner with the Community Foundation on your client’s charitable lead trust

Charitable lead trusts require coordinated planning across multiple disciplines. As the advisor closest to your client’s overall financial picture, you are best positioned to identify candidates for this strategy and initiate the planning conversation. We recommend discussing CLT potential with your client’s tax advisor and estate planning attorney as a first step.

Greater Houston Community Foundation can serve as a resource throughout this process. We regularly partner with professional advisors to implement CLTs and other high-level charitable strategies. Our team can provide educational materials for client conversations, model the DAF component of CLT structures, assist with the administrative aspects of receiving CLT payments, and offer guidance on effective grantmaking strategies.

If you have clients who might benefit from charitable lead trust planning, we welcome the opportunity to collaborate with you and their other advisors. Ready to get started? Call us at 713-333-2210 or reach out directly to schedule a conversation.

More Helpful Articles by Greater Houston Community Foundation:

- How to Start a Scholarship Fund

- Charitable Deduction Carry Forward: Making the Most of Your Donation

- How To Maximize Charitable Deductions

- Donating Art to Charity: Rules, Valuations, and Tax Benefits

- The Importance of Charitable Giving In Financial Planning

This website is a public resource of general information that is intended, but not promised or guaranteed, to be correct, complete and up to date. The materials on this website, including all comments and responses to comments, do not constitute legal, tax, or other professional advice, and is not intended to create, and receipt or viewing does not constitute, nor should it be considered an invitation for, an attorney-client relationship. The reader should not rely on information provided herein and should always seek the advice of competent legal counsel and/or a tax professional in the reader’s state or jurisdiction. The owner of this website does not intend links on the website to be referrals or endorsements of the linked entities.