Guide to Charitable Remainder Trusts

For individuals with appreciated assets who want to generate income, support charitable causes, and reduce their tax burden, charitable remainder trusts (CRTs) can offer a powerful planning opportunity. These specialized irrevocable trusts allow you to convert low-yielding or highly appreciated assets into income streams while securing meaningful tax deductions and ultimately benefiting the charities you care about most.

The catch is that charitable remainder trusts are inherently high-complexity. Unlike simpler giving strategies, setting up and administering charitable remainder trusts requires deep collaboration between your estate planning attorneys, tax planners, and philanthropic advisors. For donors in the right situation—particularly when you own appreciated property that generates little current income—the financial and charitable benefits of setting up a CRT can be transformative.

Continue reading to learn how charitable remainder trusts function, their advantages and limitations, and whether this strategy might align with your financial and philanthropic goals. Or call us at 713-333-2210 to discuss with our planning team.

Key Insights

- Charitable remainder trusts allow you to convert appreciated assets into income streams, bypass capital gains tax, and receive immediate income tax deductions.

- CRTs can be structured as either annuity trusts that pay a fixed dollar amount annually or unitrusts that pay a percentage of annually revalued assets, offering inflation protection and growth potential.

- The charitable remainder interest must equal at least 10% of the initial trust value, preventing donors from selecting payout rates that would exhaust the trust before charity receives anything.

- Pairing a CRT with a donor advised fund as the remainder beneficiary can provide flexibility to adjust charitable priorities over time without trust amendments while enabling multi-generational family involvement in philanthropy.

- CRTs generally make economic sense only for funding amounts of $250,000 or more due to setup costs and ongoing administration expenses including annual tax return preparation, trustee fees, and investment management costs.

Table of Contents

- What are the two types of charitable trusts?

- How does a charitable remainder trust work?

- Benefits of charitable remainder trusts

- Potential pitfalls of charitable remainder trusts

- Pairing a trust with a DAF

- Charitable remainder trust FAQs

- Partner with the Community Foundation on your charitable remainder trust

What are the two types of charitable trusts?

While there are countless variations on the charitable trust model, there are essentially two fundamental structures. Each of these trust types serves quite different planning objectives; they both involve irrevocable trusts that benefit charity, but they operate as mirror images of each other in terms of when charity receives its benefit.

Charitable lead trusts

Charitable lead trusts (CLTs) direct income to charitable organizations for a specified period, with the remaining assets eventually passing to family members or other non-charitable beneficiaries. These trusts are particularly effective for transferring wealth to heirs while reducing gift and estate taxes, as charity receives its benefit first during the trust term.

Continue reading about how charitable lead trusts work

Charitable remainder trusts

In contrast, charitable remainder trusts provide income to you or designated beneficiaries first, with the remaining trust assets passing to charity after the income term concludes. This structure prioritizes current income generation and immediate tax deductions while planning for charitable support in the future. CRTs are the focus of this guide and are one of the most popular planned giving vehicles for donors with significant appreciated assets seeking both personal financial benefits and philanthropic impact.

How does a charitable remainder trust work?

Charitable remainder trusts follow a three-phase structure that unfolds over many years, sometimes spanning decades, depending on how the trust is configured.

Phase 1: Funding the charitable remainder trust

The process begins when you transfer assets into an irrevocable trust. Ideal funding assets often include highly appreciated securities, income-producing real estate, closely held business interests, or other property that has experienced significant growth in value. Unlike keeping the asset and selling it yourself, transferring it to a CRT and having the trustee sell it allows the trust to bypass capital gains tax on the sale, preserving the full asset value for reinvestment.

Once established, it becomes an irrevocable gift, you cannot revoke the trust or reclaim the transferred assets. This permanence is what generates the tax benefits, but it also means you need to plan carefully before making the transfer.

Phase 2: Taking income distributions

After the trust is funded and assets are sold or repositioned, the trust begins making regular income payments to you or other named beneficiaries. These distributions continue for a defined period—either for the lifetime of one or more individuals, or for a specific term.

The trust can be structured in one of two ways:

- Charitable remainder annuity trust (CRAT): This version pays a fixed dollar amount each year, calculated as a percentage of the initial trust value. The payment remains constant regardless of investment performance.

- For example, a 5% CRAT funded with $1,000,000 would distribute $50,000 annually throughout the trust term, providing predictable income but no adjustment for inflation or investment growth.

- Charitable remainder unitrust (CRUT): This alternative pays a fixed percentage of the trust’s value as recalculated each year. If the trust grows through successful investments, income payments increase accordingly.

- Using the same example, a 5% CRUT initially valued at $1,000,000 would pay $50,000 in year one, but if the trust grows to $1,200,000 in year two, the payment would increase to $60,000. This structure provides inflation protection and growth potential but introduces payment variability.

The payout percentage must fall between 5% and 50%, with most trusts selecting rates between 5% and 8% to balance current income needs against long-term growth and charitable remainder value.

Phase 3: Charitable distributions

When the income term concludes—whether due to the passing of all income beneficiaries or the expiration of a fixed term—the remaining trust assets pass to the charitable organizations you designated when establishing the trust. This remainder distribution completes the trust’s purpose and delivers the charitable benefit that justified the original tax deduction.

Many donors choose to name community foundations like Greater Houston Community Foundation as the remainder beneficiary, often directing distributions to a donor advised fund that allows family members to continue recommending grants to operating charities even after the trust terminates.

Benefits of charitable remainder trusts

For donors in the right circumstances, charitable remainder trusts offer a powerful combination of financial and philanthropic advantages that are difficult to replicate through other strategies.

| Immediate income tax deduction |

| When you fund a CRT, you qualify for an immediate income tax deduction based on the calculated present value of the future charitable remainder. This deduction reflects the portion of the trust that will eventually pass to charity, accounting for the trust term, payout rate, and IRS interest rate assumptions. The deduction can significantly reduce your current tax liability, though it must fall within charitable giving deduction limits that restrict deductions to a percentage of your adjusted gross income. |

| Capital gains tax bypass |

| Perhaps the most powerful benefit of a CRT is the ability to sell appreciated assets without triggering capital gains tax. When the trust sells appreciated property, no tax is due at the trust level, allowing the full proceeds to be reinvested and generate income. This advantage is particularly valuable for donors holding low-basis stock, investment real estate, or business interests that would face substantial taxation if sold directly. |

| Enhanced income potential |

| Many donors fund CRTs with appreciated assets that currently generate little or no income—like growth stocks, raw land, or artwork. After the trust sells these assets tax-free and reinvests the proceeds in income-producing investments, the donor can benefit from a substantial increase in cash flow. This makes CRTs particularly attractive for pre-retirees who need to convert growth-oriented holdings into retirement income. |

| Estate tax reduction |

| Assets transferred to a CRT are removed from your taxable estate, potentially reducing estate tax liability for individuals with estates subject to federal estate taxes. The charitable remainder that will eventually pass to charity receives a full estate tax deduction, further reducing the tax burden on your heirs. |

Beyond the financial and tax benefits of charitable donations, CRTs allow you to make a significant charitable contribution that might not be possible through outright giving. The trust structure converts an appreciated asset you might have held for life into meaningful charitable support, creating a lasting legacy that reflects your values and priorities.

What are the pitfalls of a charitable remainder trust?

While CRTs offer substantial benefits, they also come with limitations and potential drawbacks that donors should carefully consider before proceeding.

| Irrevocability and loss of control |

| Once you transfer assets to a CRT, you cannot change your mind. The transfer is permanent, and you surrender legal ownership of the property. While you receive income from the trust, you cannot access the principal for emergencies or changed circumstances. This often makes CRTs less suitable for donors who might need access to the transferred assets down the line. |

| Complexity and administrative costs |

| Establishing a CRT requires professional legal drafting, typically costing several thousand dollars. The trust must file annual tax returns, requires professional administration, and may incur trustee fees that reduce net income to beneficiaries. These ongoing costs can be substantial, which is why CRTs generally make sense only for transfers of hundreds of thousands or more. |

| No capital gains elimination for distributions |

| While the trust itself doesn’t pay capital gains tax when it sells appreciated assets, those gains don’t disappear entirely. Under complex “tier” rules, trust income distributed to beneficiaries carries out the trust’s taxable income, including capital gains. Depending on the trust’s earnings and your tax situation, some or all of the income you receive may be subject to ordinary income tax, capital gains tax, or other taxation. |

Additional considerations apply for older donors who need uniquely high payout percentages, those who need shorter trust terms, or those looking to fund accounts with retirement account funds.

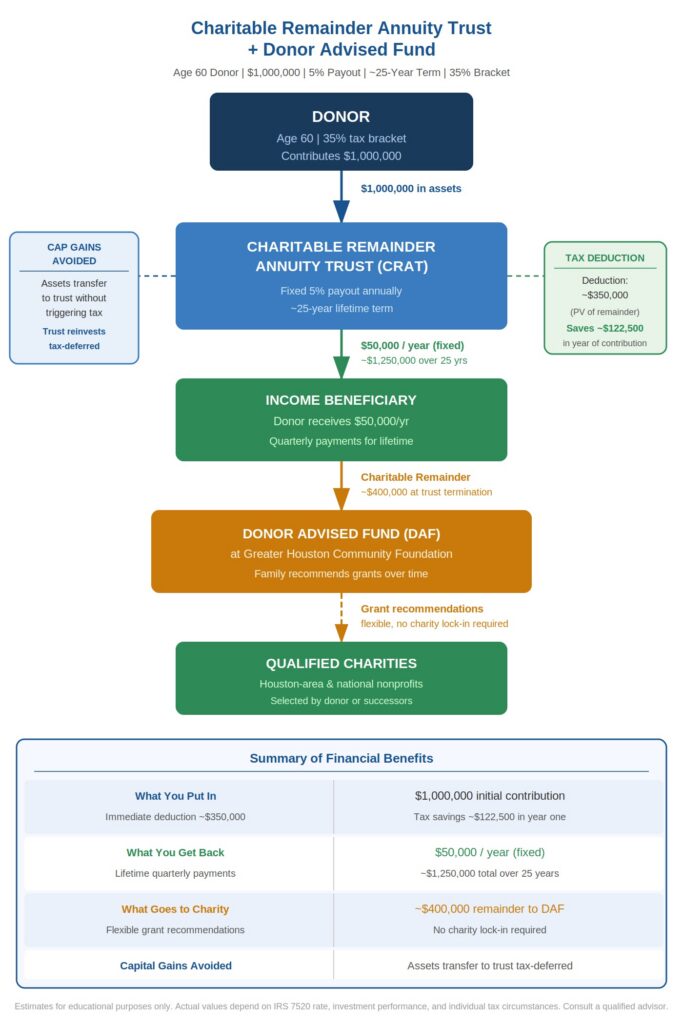

Charitable remainder trust example: pairing with a DAF

One particularly effective implementation strategy involves naming a donor advised fund at Greater Houston Community Foundation as the charitable remainder beneficiary of a CRT. This approach addresses a common concern: uncertainty about which specific charities to support many years into the future.

Consider a 60-year-old donor who establishes a CRAT that will pay income for her lifetime and then distribute the remainder to charity. Rather than naming specific operating charities now—organizations that may not exist or align with her priorities decades from now—she names her DAF as the trust beneficiary.

Here’s how this works in practice:

- During her lifetime, she receives yearly payments from the CRT, providing retirement cash flow and enjoying the immediate tax deduction based on the projected charitable remainder.

- At trust termination, the trust distributes its remaining assets to her donor advised fund at the Community Foundation. For donors interested in understanding this vehicle better, our guide on what is a donor advised fund explains how these accounts function.

- The donor’s children or other successor advisors can then recommend grants from the DAF to operating charities, allowing the family’s philanthropic legacy to continue and adapt to changing community needs over time.

- If charitable priorities shift, the DAF structure allows grant recommendations to reflect current interests without requiring trust amendments or legal modifications.

This delivers both the financial benefits of the CRT during the donor’s lifetime and the flexibility of a DAF for the charitable distribution phase, creating a solution that balances personal and philanthropic needs. The tax advantages can be substantial: beyond the immediate deduction when establishing the trust, the DAF structure can provide ongoing deductions as successors make additional contributions, creating multi-generational tax efficiency.

Here’s what this might look like with $1,000,000 initial funding, a 5% payout, and a ~25 year term:

Continue reading about donor advised fund tax deductions

Charitable remainder trust FAQs

What is the charitable remainder trust 10 percent rule?

The 10 percent rule, formally known as the “minimum remainder” requirement, mandates that the actuarially calculated value of the charitable remainder must equal at least 10% of the initial trust value. The rule is intended to prevent donors from selecting payout rates so aggressive that they risk exhausting the trust before charity receives anything.

How much does it cost to set up a charitable remainder trust?

The initial legal drafting and establishment of a CRT costs thousands of dollars, escalating based on complexity and whether the trust involves multiple beneficiaries, special provisions, or sophisticated asset transfers. This covers attorney fees for drafting the trust document, reviewing asset titles, and coordinating the initial funding.

Beyond setup costs, ongoing administration expenses include annual tax return preparation, trustee fees, and investment management costs if applicable. These recurring expenses mean that CRTs generally make economic sense only for initial funding amounts of $250,000 or more, though some donors establish trusts with smaller amounts if their charitable and income objectives justify the proportionally higher costs.

How do CRTs compare to private foundations?

Both CRTs and private family foundations allow substantial charitable gifts with tax benefits, but they serve different purposes. Private foundations provide ongoing control over grantmaking and can continue indefinitely across generations, while CRTs primarily serve as income and estate planning tools that terminate after distributing the remainder to charity.

Private foundations face strict regulatory requirements, minimum annual distribution rules (5% of assets), and excise taxes on investment income. CRTs avoid these constraints but require income distributions to beneficiaries and ultimately transfer all assets to charity. For families seeking permanent control, a private family foundation may be more appropriate, while those prioritizing income generation and capital gains avoidance often find CRTs more suited to their needs.

Partner with the Community Foundation on your charitable remainder trust

Establishing a charitable remainder trust requires extensive planning and coordination between legal, tax, and philanthropic advisors, but for the right donors, the benefits can be transformative.

Our planned giving team regularly collaborates with professional advisors to structure CRTs that name the Community Foundation or donor advised funds as remainder beneficiaries. We can provide illustrations showing projected income streams and tax benefits, coordinate with your attorney on trust language that preserves flexibility for charitable designations, offer guidance on effective grantmaking strategies if your CRT ultimately benefits a DAF, and help ensure seamless administration when the trust eventually distributes its remainder to charitable purposes.

Whether you’re exploring a CRT for the first time or ready to move forward with implementation, we’re here to help you navigate this powerful planning tool.

To discuss whether a charitable remainder trust might benefit you and your family, call Greater Houston Community Foundation at 713-333-2210 or reach out directly to schedule a conversation.

More Helpful Articles by Greater Houston Community Foundation:

- How Do Corporate Philanthropy Programs Work?

- What Are Qualified Charitable Distributions?

- What is a Legacy Fund?

- Wealth Preservation with Charitable Giving: The Generation-Skipping Transfer Tax

- How to Start a Scholarship Fund

This website is a public resource of general information that is intended, but not promised or guaranteed, to be correct, complete and up to date. The materials on this website, including all comments and responses to comments, do not constitute legal, tax, or other professional advice, and is not intended to create, and receipt or viewing does not constitute, nor should it be considered an invitation for, an attorney-client relationship. The reader should not rely on information provided herein and should always seek the advice of competent legal counsel and/or a tax professional in the reader’s state or jurisdiction. The owner of this website does not intend links on the website to be referrals or endorsements of the linked entities.